Congratulations! Whether this is your first time buying a home or you’re refinancing your existing home loan, you’re making a great choice — and Planet Home Lending will be your partner every step of the way.

This blog walks you through the mortgage loan process from beginning your application all the way to closing and funding your loan. We make it easy to understand because Planet’s goal is to empower you to make the best mortgage choices for your unique needs and access all the benefits of homeownership.

Before you begin the mortgage loan process, feel free to visit our mortgage loan calculators and get a general idea of how your numbers look — the affordability calculator can even show you if a monthly mortgage payment could be lower than your rent based on the home purchase price.

The mortgage loan process begins with your application. The Uniform Residential Loan Application, or URLA, is designed to make sure everyone is on the same page — literally. It may look long, but don’t be intimidated! All your documentation falls into four simple categories: Income and Employment, Assets, Credit History, and Property.

Planet makes applying for a mortgage easy. You may choose to apply in person at one of our many branches, or via our secure online portal. In fact, if you have your financial information at hand, the mortgage application process can take less than an hour.

These two mortgage loan process steps — home appraisals and home inspections — may sound the same, but they’re different. An appraisal is a professional evaluation of how much your home is worth. A home inspection checks for problems and identifies repairs your home might need.

While you can choose your own home inspector, your appraiser is assigned by the appraisal management company, and the buyer typically pays this fee. Appraisers are licensed independent third parties and federal law forbids Planet loan officers from attempting to influence the appraiser or the home valuation.

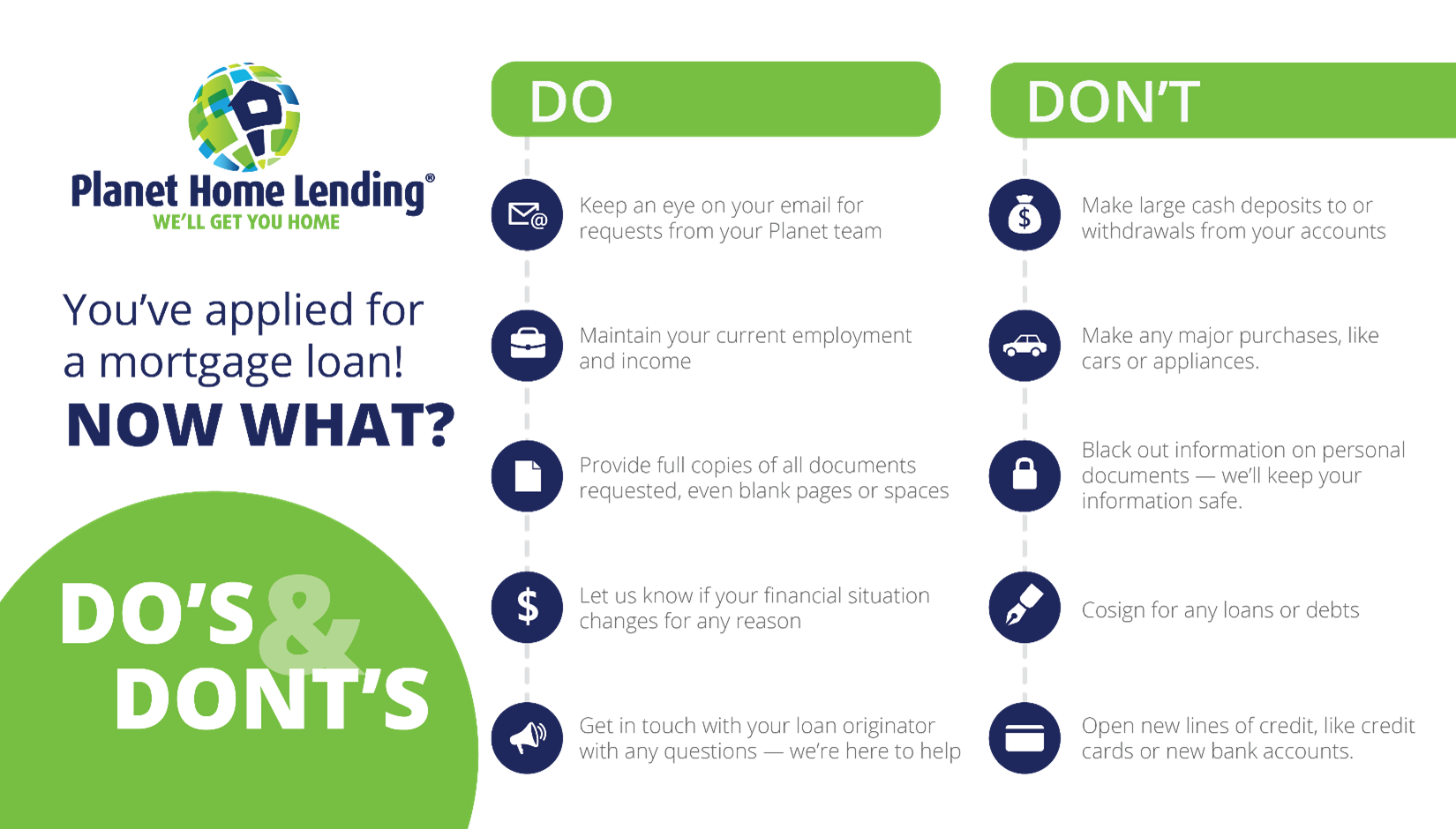

While processing your mortgage loan, your Planet processor makes sure the correct documents are collected, verified, and placed in your loan file to be ready for underwriting. They order and analyze your credit report looking for inaccuracies, and keep track of the various mortgage deadlines.

Once they have everything in order, they hand your file off to the underwriting professionals.

The mortgage underwriting process is the close examination of your finances to determine if you have the resources to pay your mortgage loan. The law requires us to verify certain aspects of your application. We want to make sure your home loan suits your financial situation. Everyone has the same goal, which is making sure you can pay back your loan and enjoy many happy years in your home.

Because underwriting is so detailed, it can take as little as two to three days or over a week. It is also common for the underwriter to request additional information, such as a letter from a family member who gifted you money for a down payment. If that happens, you might find that you receive a conditional approval.

Conditional approval means that your underwriter has verified your information and is fairly certain that you qualify for your mortgage loan, but there are some things that need clarification. At this point, Planet may ask you to send more information.

Don’t panic! This is very common in the mortgage approval process, and your Planet mortgage loan originator or loan processor will be in touch with exactly what you need to provide.

You’ve been through the final review, you’ve handled any additional requests, and the underwriter has verified that you are ready to head to the closing table. Well done!

Planet will send you a Closing Disclosure at least three business days before your closing is scheduled. Remember the Initial Loan Estimate you signed at the beginning of your mortgage application? This five-page document will look similar, but it lays out the final details of your mortgage: your loan terms, interest rate, loan amount, projected monthly payments, and how much you will pay in fees at the closing table to get your loan, also known as closing costs.

Then it’s time to meet with your title company in person or remotely to sign the documents that give you a home loan. If you’re buying a home, at this time you’ll also receive the title to your new home. Make sure you bring the following so the signing can go smoothly:

✓ A valid, government-issued ID

✓ A cashier’s check, available from your bank to pay your closing costs, unless you have wired the funds in advance

What is funding a mortgage? Funding is when we wire the money for your home purchase to the title company or to pay off your current mortgage in a refinance. It’s the final step in the mortgage loan process.

Different states have different regulations covering funding, and your Planet mortgage professional can tell you when your loan will fund.

At Planet, our motto is, “We’ll get you home.” And we chose it with care. Whether you’re buying or refinancing, cashing out your home’s equity or investing in real estate, our goal is to be the best mortgage lender for your needs. Reach out any time with questions — because when we say we'll get you home, we mean it.

With Planet at your side, you can live confidently through a lending process that is committed to unrivaled quality and guided by a truly local perspective. We are your neighbors and members of the community you call home, all part of a nationwide team of experienced and dedicated professionals that prioritize service and borrower success above all else.

© 2024 Planet Home Lending LLC NMLS ID#17022

© 2024 Planet Home Lending LLC NMLS ID#17022